Gout Biologics Trend Review

Current Trends in Gout Biologics: Pegloticase and Emerging Next-Generation Uricase Therapies

Overview of Gout Biologics

The therapeutic landscape for gout has undergone remarkable transformation over the past two decades, evolving from reliance on small-molecule drugs with limited efficacy and significant toxicities to sophisticated biologic interventions targeting specific disease mechanisms. This shift reflects broader trends in rheumatology and immunology, where biologics have revolutionized the management of autoimmune and inflammatory conditions.

The gout biologics market encompasses two primary categories: agents targeting inflammatory cytokines for acute flare management (IL-1β inhibitors) and agents targeting uric acid metabolism for chronic disease modification (urate-lowering biologics). While IL-1β inhibitors such as canakinumab and anakinra address the inflammatory manifestations of gout, uricase-based therapies represent the only biologic approach to correcting the underlying metabolic defect—hyperuricemia.

The global gout therapeutics market, valued at approximately $4.24 billion in 2025, is projected to reach $6.67 billion by 2031, driven by rising disease prevalence, increasing recognition of undertreatment, and the introduction of novel agents. Within this market, biologics currently represent a niche segment focused on refractory patients, but their share is expected to grow as next-generation products address current limitations and expand eligible populations.

gout biologics trends, pegloticase market, uricase pipeline, biologics gout therapy, next generation uricase

1. Market Landscape

The contemporary gout treatment market is characterized by a hierarchy of interventions stratified by disease severity, treatment history, and cost considerations.

| Segment | Representative Agents | Market Share | Growth Trajectory | Key Drivers |

|---|---|---|---|---|

| Xanthine oxidase inhibitors | Allopurinol, febuxostat | ~60% | Stable (generic competition) | First-line standard; low cost |

| Uricosurics | Probenecid, benzbromarone | ~10% | Declining | Limited efficacy; safety concerns |

| IL-1β inhibitors (acute) | Canakinumab, anakinra | ~5% | Moderate | Refractory acute gout; high cost |

| Uricase biologics | Pegloticase | ~3% | Growing (next-gen pipeline) | Refractory chronic gout; unmet need |

| Emerging therapies | SEL-212, AR882, D-0120 | <1% | High growth potential | Innovation; improved profiles |

1.1 Pegloticase Market Position

Pegloticase, Recombinant Uricase (Krystexxa®) currently dominates the uricase biologic segment as the only FDA-approved agent for chronic refractory gout. Since its 2010 approval, pegloticase has established a clinical niche in the most challenging patients—those with severe tophaceous gout unresponsive to conventional therapy. However, its market penetration has been limited by immunogenicity concerns, infusion requirements, and high cost (approximately $5,000-$6,000 per infusion, with annual costs exceeding $100,000).

Horizon Therapeutics (now part of Amgen) has implemented strategies to expand pegloticase utilization, including:

- Co-promotion agreements with rheumatology networks

- Patient assistance programs and reimbursement support

- Development of methotrexate co-therapy protocols to improve response rates

- Education initiatives highlighting treat-to-target benefits

Despite these efforts, pegloticase remains prescribed for only a fraction of eligible patients, with estimates suggesting <10% of refractory gout patients receive uricase therapy.

2. Pegloticase Positioning

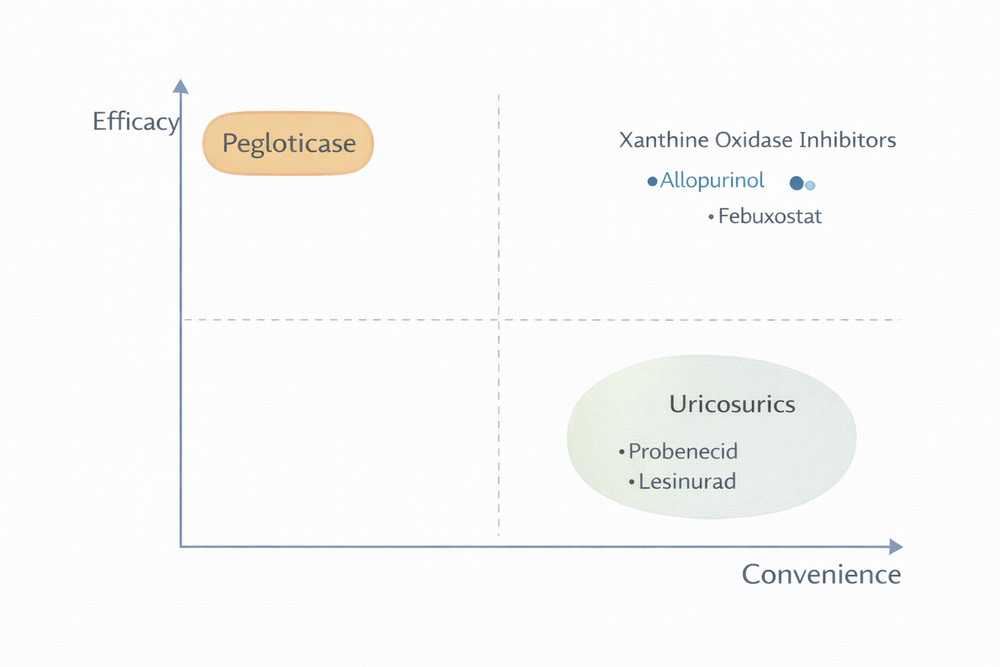

Within the biologics landscape, pegloticase occupies a unique position as the only agent capable of achieving profound, rapid urate lowering in refractory patients. Its clinical profile is characterized by:

2.1 Strengths

- Unique mechanism (enzymatic degradation vs. synthesis inhibition)

- Rapid onset (hours vs. weeks for oral agents)

- Profound magnitude of effect (serum urate often <1 mg/dL)

- Efficacy in advanced chronic kidney disease

- Demonstrated tophus resolution and functional improvement

2.2 Limitations

- High immunogenicity (40-60% treatment failure due to ADAs)

- Intravenous administration requirement

- Risk of severe infusion reactions

- High cost and healthcare resource utilization

- Limited duration of response in many patients

Fig 1. Market positioning map showing pegloticase relative to other gout therapies on efficacy vs. convenience axes

The current clinical development focus centers on mitigating these limitations through combination therapy (methotrexate co-administration) and next-generation formulations rather than displacing pegloticase entirely.

3. Pipeline Drugs

The gout biologics pipeline is robust, with several promising candidates in advanced clinical development targeting improved efficacy, reduced immunogenicity, or enhanced convenience.

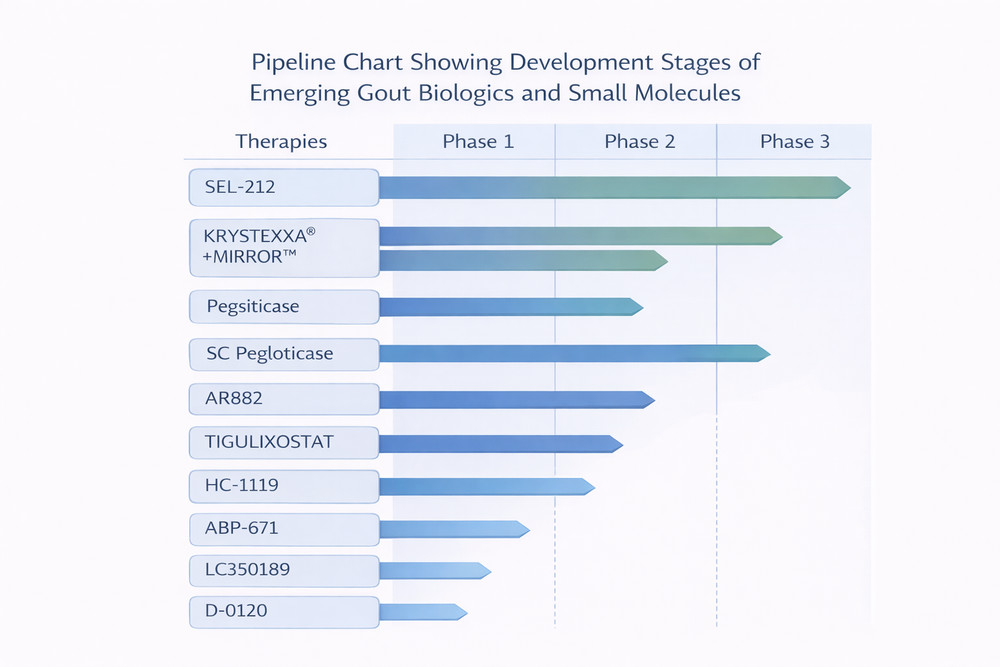

3.1 SEL-212 (Selecta Biosciences/Sobi)

SEL-212 represents the most advanced next-generation uricase, combining pegadricase (a PEGylated recombinant uricase from Candida utilis) with ImmTOR nanoparticles. The ImmTOR component contains rapamycin (sirolimus) encapsulated in biodegradable nanoparticles that induce immune tolerance by targeting antigen-presenting cells and promoting regulatory T-cell responses.

| Trial | Phase | Design | Key Results | Status |

|---|---|---|---|---|

| COMPARE | 3 | Head-to-head vs. pegloticase | Superior sustained response; reduced ADAs | Completed; positive results |

| DISSOLVE I & II | 3 | Two replicate trials in uncontrolled gout | Primary endpoint met; improved safety | Completed; regulatory submission planned |

The COMPARE trial demonstrated that SEL-212 achieved higher response rates than pegloticase alone, with the immune tolerance induction significantly reducing anti-drug antibody formation. If approved, SEL-212 could capture substantial market share from pegloticase by offering improved efficacy and safety profiles.

3.2 AR882 (Arthrosi Therapeutics)

While not a biologic, AR882 is a novel small-molecule URAT1 inhibitor with potential to compete in the refractory gout space. This agent demonstrates high potency and selectivity for the urate transporter, achieving substantial uricosuric effects. Phase 3 data showed 50% complete tophus resolution at 12 months, with FDA Fast Track designation granted in August 2024. The oral formulation offers convenience advantages over intravenous uricase, though it lacks the rapid, profound urate lowering of enzymatic therapy.

3.3 Other Pipeline Candidates

- D-0120 (Dotinurad): Selective URAT1 inhibitor in Phase 3; potential for combination with XOIs

- Ulodesine (BCX4208): Purine nucleoside phosphorylase inhibitor; reduces uric acid production through alternative pathway

- Ruzinurad: Dual URAT1/OAT4 inhibitor; enhanced uricosuric efficacy

Fig 2. Pipeline chart showing development stages of emerging gout biologics and small molecules

4. Innovation Trends

Several key innovation trends are shaping the future of gout biologics development:

4.1 Immunogenicity Mitigation

The recognition that anti-drug antibodies represent the primary limitation of uricase therapy has catalyzed diverse approaches to immune tolerance induction. Beyond the ImmTOR nanoparticles employed in SEL-212, strategies under investigation include:

- Plasmacytoid dendritic cell-targeted tolerogenic vaccines

- Regulatory T-cell expansion protocols

- Low-dose IL-2 therapy to promote immune tolerance

- HLA-matched peptide epitope modification to reduce T-cell recognition

4.2 Alternative Polymer Conjugation

Research into alternatives to PEG aims to retain pharmacokinetic benefits while avoiding anti-PEG antibodies. Polysarcosine, poly(2-oxazoline), and polypeptoid conjugates are advancing through preclinical development, with some candidates demonstrating comparable half-life extension and potentially reduced immunogenicity.

4.3 Gene Therapy

Long-term solutions may involve in vivo gene delivery of functional uricase using adeno-associated viral (AAV) vectors or lipid nanoparticles. Preclinical studies have demonstrated sustained uricase expression and urate lowering in animal models, potentially offering permanent correction of the metabolic defect without repeated protein administration. Challenges include immune responses to viral vectors, optimal tissue targeting (liver vs. muscle), and durability of expression.

4.4 Personalized Medicine

Pharmacogenomic approaches to predict immunogenicity risk and optimize patient selection are emerging. HLA typing, anti-PEG antibody screening, and gene expression profiling may enable identification of patients most likely to respond to uricase therapy, improving the risk-benefit ratio and justifying treatment costs.

5. Investment Insights

The gout biologics sector presents attractive investment opportunities driven by unmet medical need, premium pricing potential, and innovation catalysts.

5.1 Market Drivers

- Aging populations with increasing gout prevalence

- Growing recognition of gout as a serious, undertreated disease with cardiovascular and renal comorbidities

- Failure of 30-50% of patients to achieve target urate with conventional therapy

- Premium pricing supported by orphan-drug-like positioning in refractory populations

5.2 Risk Factors

- Competition from improved small molecules (URAT1 inhibitors)

- Biosimilar pressure on pegloticase as patents expire

- Safety concerns limiting physician adoption

- Reimbursement challenges for high-cost biologics

5.3 Key Investment Themes

- Next-generation uricases: SEL-212 and follow-on candidates with improved immunogenicity profiles

- Oral biologic alternatives: Small molecules achieving biologic-like efficacy (AR882)

- Combination platforms: Immunomodulatory technologies applicable across biologic classes

- Gene therapy: Long-term solutions with transformative potential

6. Future Outlook

The gout biologics market is poised for substantial evolution over the next 5-10 years. Several scenarios appear likely:

6.1 Near-term (2024-2027)

SEL-212 approval would establish a new standard of care in refractory gout, potentially displacing pegloticase in treatment-naïve biologic patients. Methotrexate co-therapy protocols may expand pegloticase utility in the interim. Oral URAT1 inhibitors will capture patients seeking convenience, though they will not fully replace uricase for severe tophaceous disease.

6.2 Medium-term (2027-2032)

Gene therapy approaches may enter clinical trials, offering the potential for definitive metabolic correction. Biosimilar pegloticase could increase access in cost-sensitive markets. Combination therapies (uricase + immunomodulator + oral ULT) may become standard for the most severe cases.

6.3 Long-term (2032+)

Personalized algorithms incorporating genetic risk stratification, biomarker monitoring, and tailored therapy selection may optimize outcomes. The distinction between "biologic" and "small molecule" gout therapy may blur as oral agents achieve biologic-like efficacy and targeted delivery systems emerge.

For researchers and drug developers, Pegloticase, Recombinant Uricase remains the foundational benchmark against which next-generation therapies are measured. Its extensive clinical experience, well-characterized pharmacology, and established manufacturing processes provide critical reference points for innovation in gout biologics.

References

1. Mordor Intelligence. (2026). Gout Therapeutics Market Size, Trends, Share & Growth Report 2031. Retrieved from https://www.mordorintelligence.com/industry-reports/gout-therapeutics-market

2. Future Market Insights. (2025). Intravenous Pegloticase Market Outlook (2025-2035). Retrieved from https://www.futuremarketinsights.com/reports/intravenous-pegloticase-market

3. Grand View Research. (2024). Gout Therapeutics Market Size, Share | Industry Report, 2030. Retrieved from https://www.grandviewresearch.com/industry-analysis/gout-therapeutics-market

4. Baraf, H. S., et al. (2024). The COMPARE head-to-head, randomized controlled trial of SEL-212 versus pegloticase for refractory gout. Rheumatology (Oxford), 63(4), 1058-1068.

5. DelveInsight. (2025). Chronic Refractory Gout Market Analysis by 2034. Retrieved from https://www.delveinsight.com/insights/chronic-refractory-gout-market-size-and-forecast

6. ACR Meeting Abstracts. (2023). Safety & Efficacy of SEL-212 in Patients with Gout Refractory to Conventional Treatment: Primary Outcomes from Two Phase 3 Studies. Arthritis & Rheumatology, 75 (suppl 9).

7. Annals of the Rheumatic Diseases. (2024). POS0260 ONCE-MONTHLY SEL-212 DEMONSTRATES EFFICACY AND SAFETY FOR UP TO 6-MONTHS IN GOUT REFRACTORY TO CONVENTIONAL THERAPY. ARD, 83(Suppl 1), 408.

8. Pharmacy Times. (2025). SEL-212 Shows Promise in Treating Chronic Refractory Gout with High Response Rates. Retrieved from https://www.pharmacytimes.com